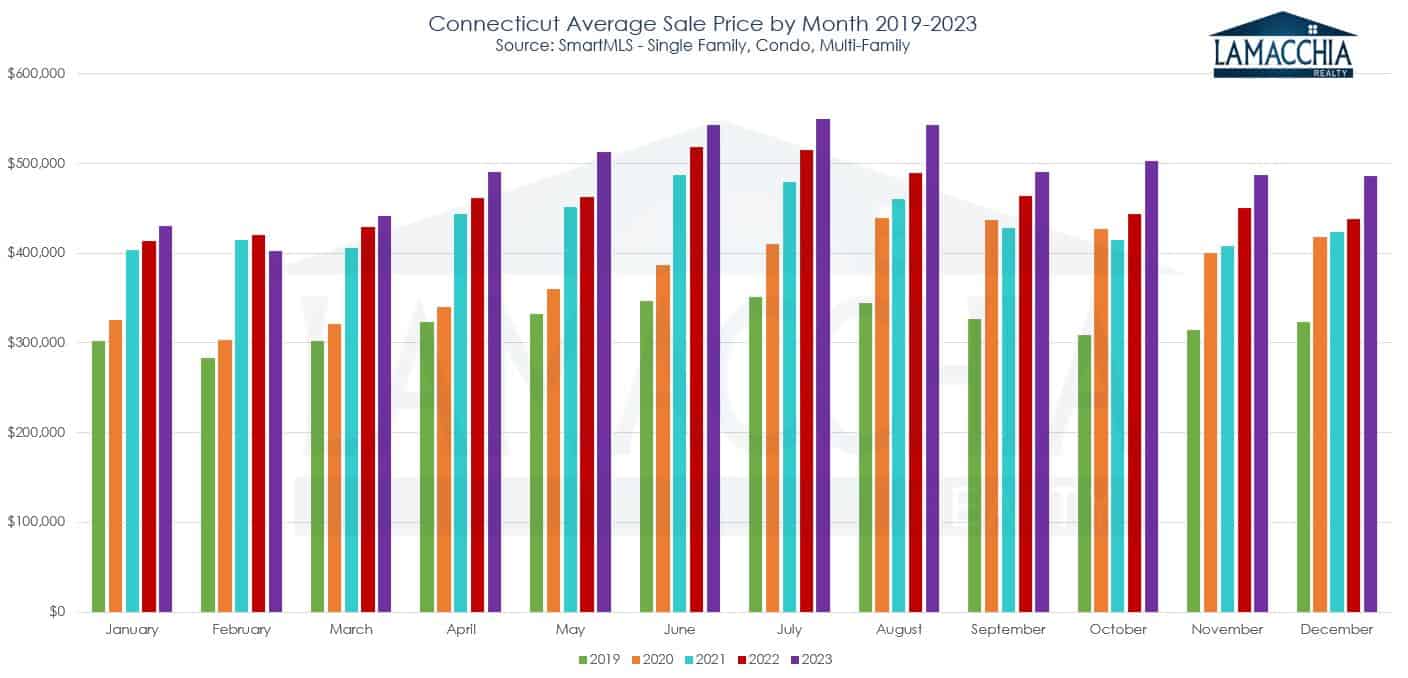

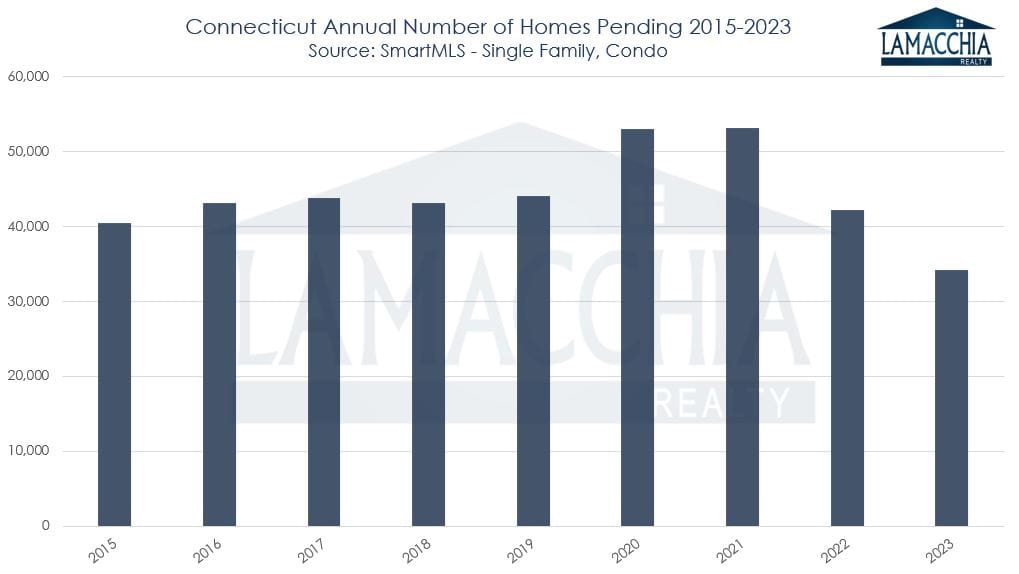

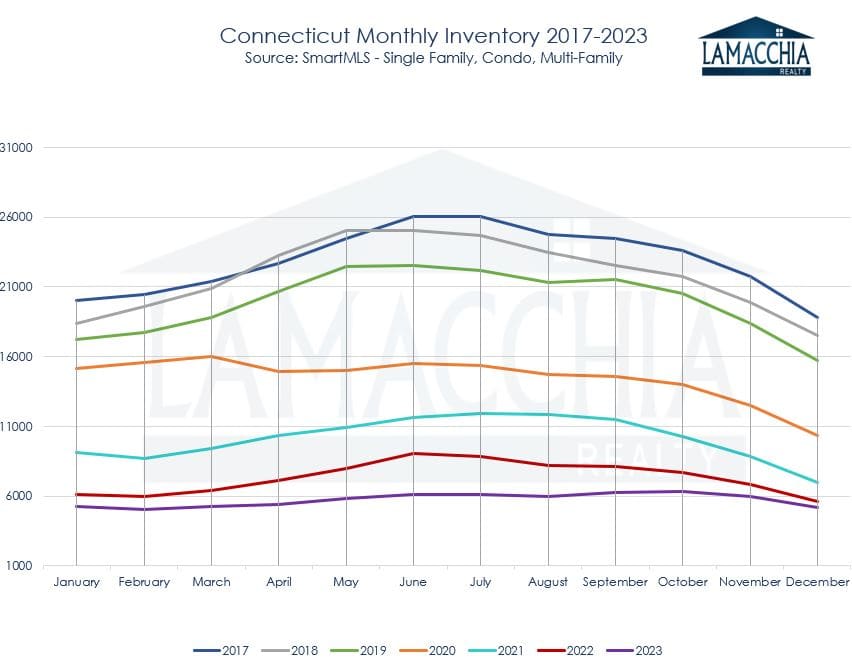

2023 stood out as a significant year in Connecticut real estate. The most notable aspect was the record-low number of homes listed, a trend not witnessed in over two decades. This created an extreme scarcity of inventory and contributed to elevated prices, but it also led to a 22% decrease in the number of sales, leaving buyers eager. As interest rates strive to find equilibrium following their sharp decline in 2020, buyers and sellers have had to accept that the era of pandemic-induced low rates is over, ushering in a period of higher monthly mortgage payments.

2023 stood out as a significant year in Connecticut real estate. The most notable aspect was the record-low number of homes listed, a trend not witnessed in over two decades. This created an extreme scarcity of inventory and contributed to elevated prices, but it also led to a 22% decrease in the number of sales, leaving buyers eager. As interest rates strive to find equilibrium following their sharp decline in 2020, buyers and sellers have had to accept that the era of pandemic-induced low rates is over, ushering in a period of higher monthly mortgage payments.

2022 also experienced a decline in sales compared to 2021 and attention-grabbing headlines raised the fear of an impending price crash. However, Anthony was very clear that was unlikely to happen. Fast forward a year, and there’s still no crash. The resilience can be attributed mostly to the decrease in inventory. The reduction in sales in 2022 was not surprising but rather a relief, considering the unsustainable frenzy of the 2021 market. The slower market activity in the following year reflects a move toward equilibrium. Despite the necessity of a market adjustment, the process can be painful, and 2023 was most certainly not comfortable for anyone involved.

This report analyzes sales, average prices, the number of active listings, and listings under contract for 2023 compared to 2022. Additionally, it predicts what’s going to happen in real estate in 2024.