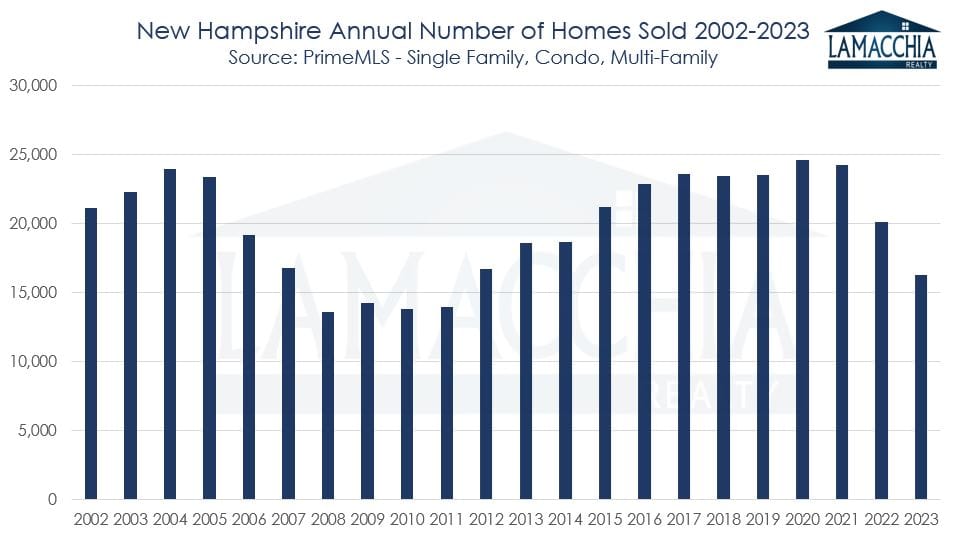

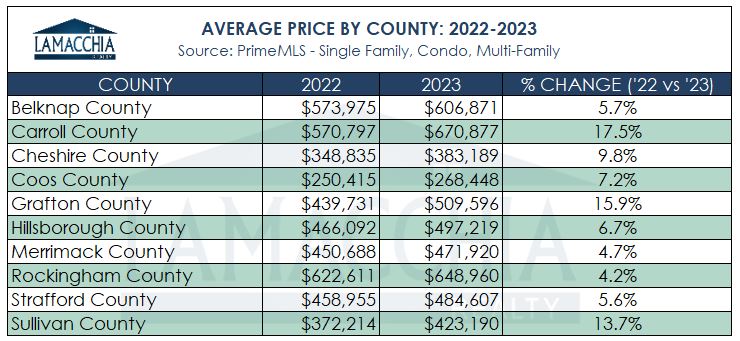

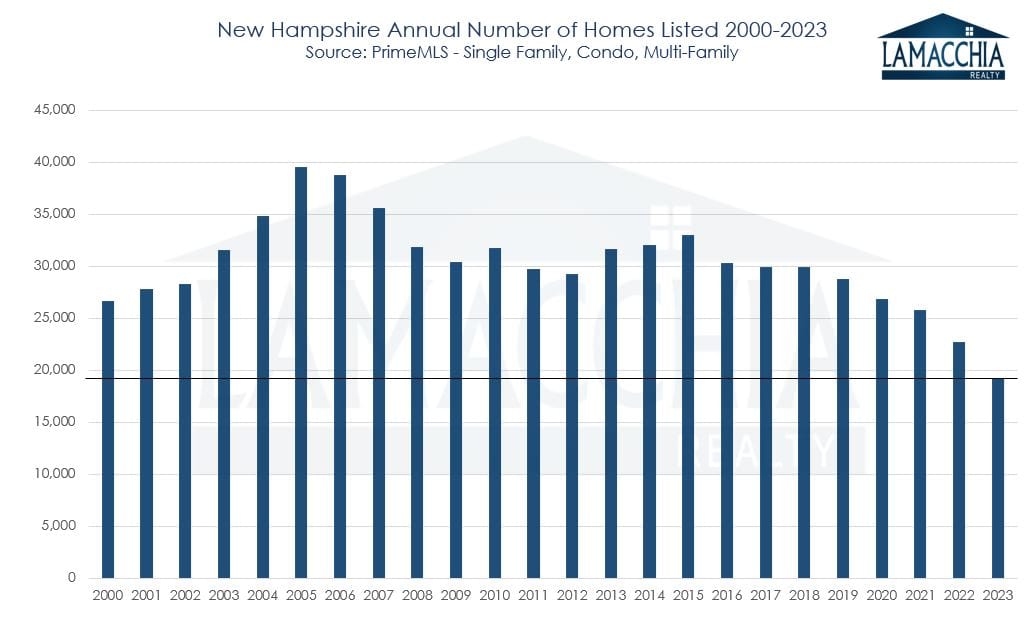

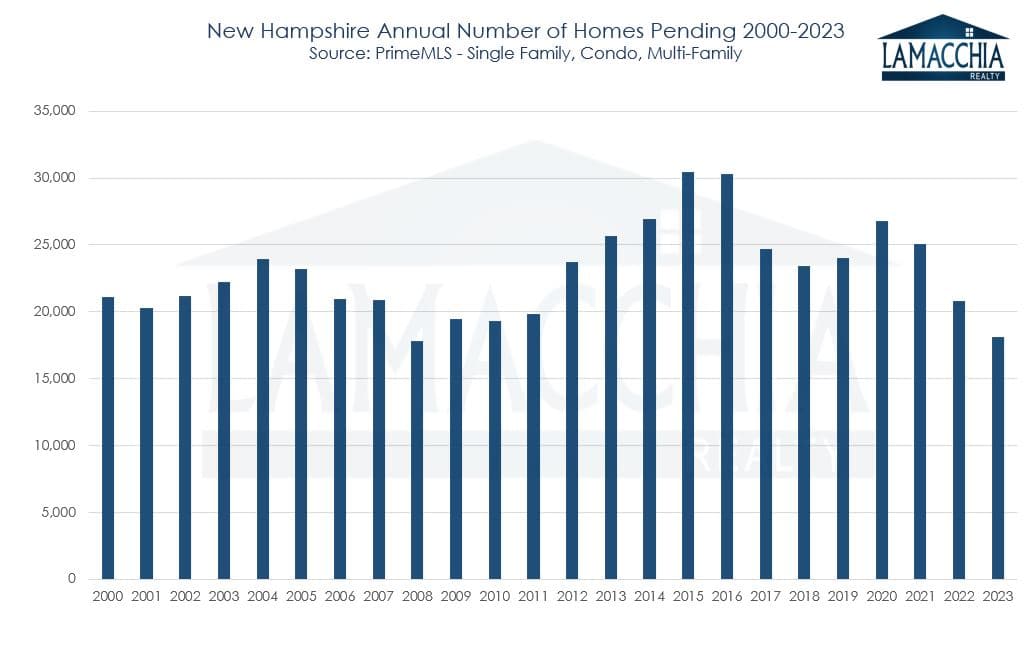

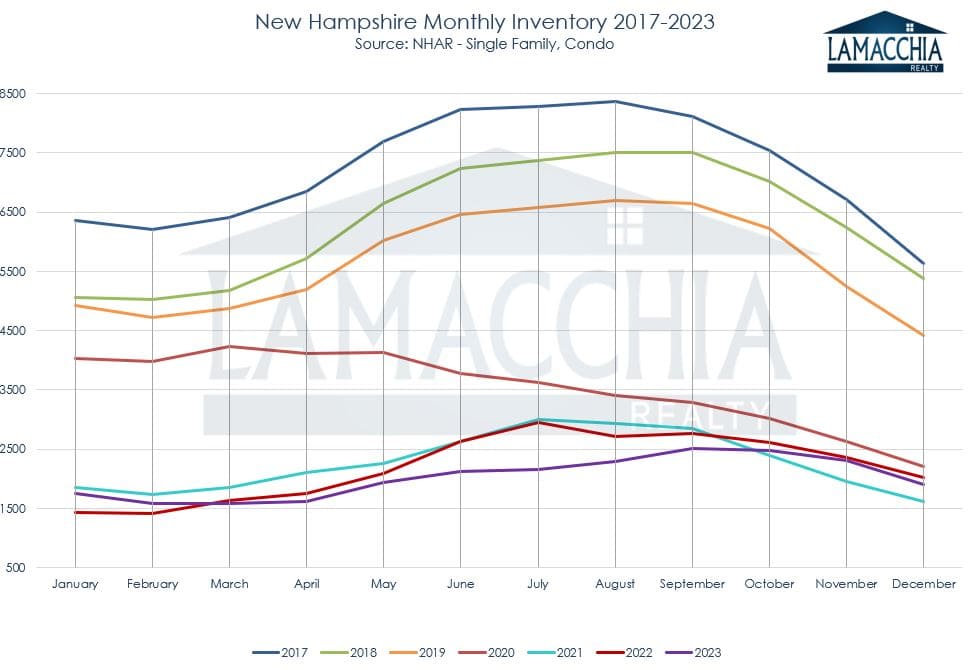

The real estate landscape witnessed significant developments in 2023, as the New Hampshire market saw a historic low in listings. This scarcity in inventory exerted upward pressure on prices, although it coincided with a 19% decline in sales. Despite this decline, motivated buyers were out there trying to secure a home while also trying to navigate lower affordability and low inventory. Sales were also down in 2022, which sparked concerns of a market crash, but as Anthony predicted, it didn’t happen, more thanks to reduced inventory rather than a decline in sales.

The real estate landscape witnessed significant developments in 2023, as the New Hampshire market saw a historic low in listings. This scarcity in inventory exerted upward pressure on prices, although it coincided with a 19% decline in sales. Despite this decline, motivated buyers were out there trying to secure a home while also trying to navigate lower affordability and low inventory. Sales were also down in 2022, which sparked concerns of a market crash, but as Anthony predicted, it didn’t happen, more thanks to reduced inventory rather than a decline in sales.

The 2022 slowdown was a welcome break from the unsustainable frenzy of 2021, and 2023 continued the trend towards balance, albeit with some challenges.

This report breaks down state-wide sales (previous years mostly covered Southern NH and the Lakes Region), average prices, the number of active listings, and how many listings went under contract for 2023 compared to 2022, and discusses what is predicted to unfold in 2024.