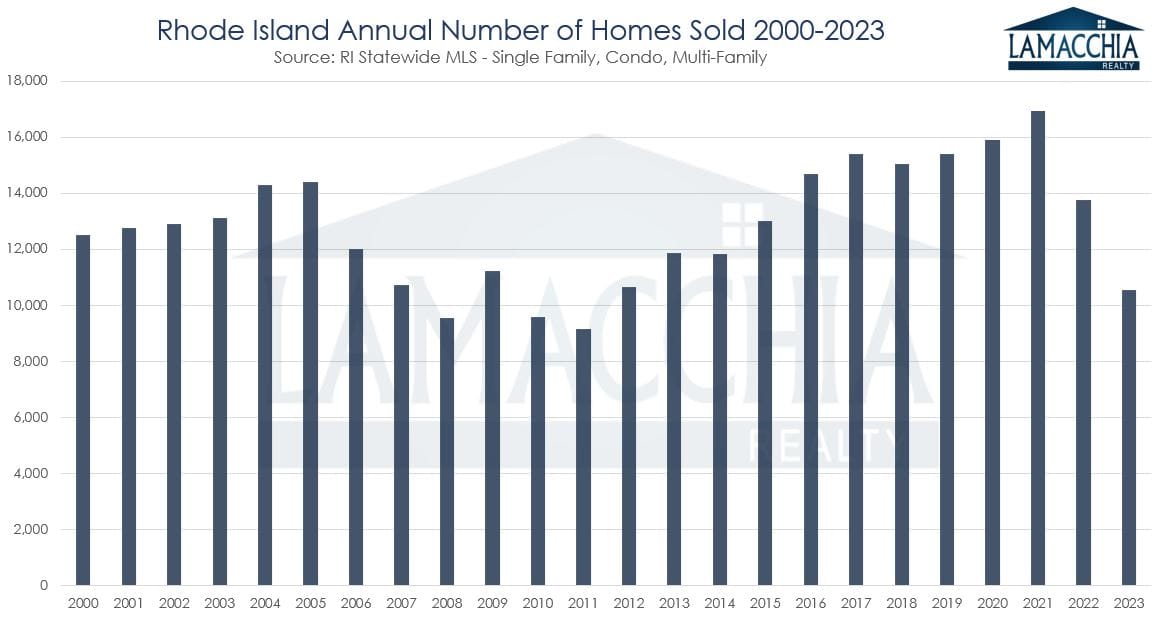

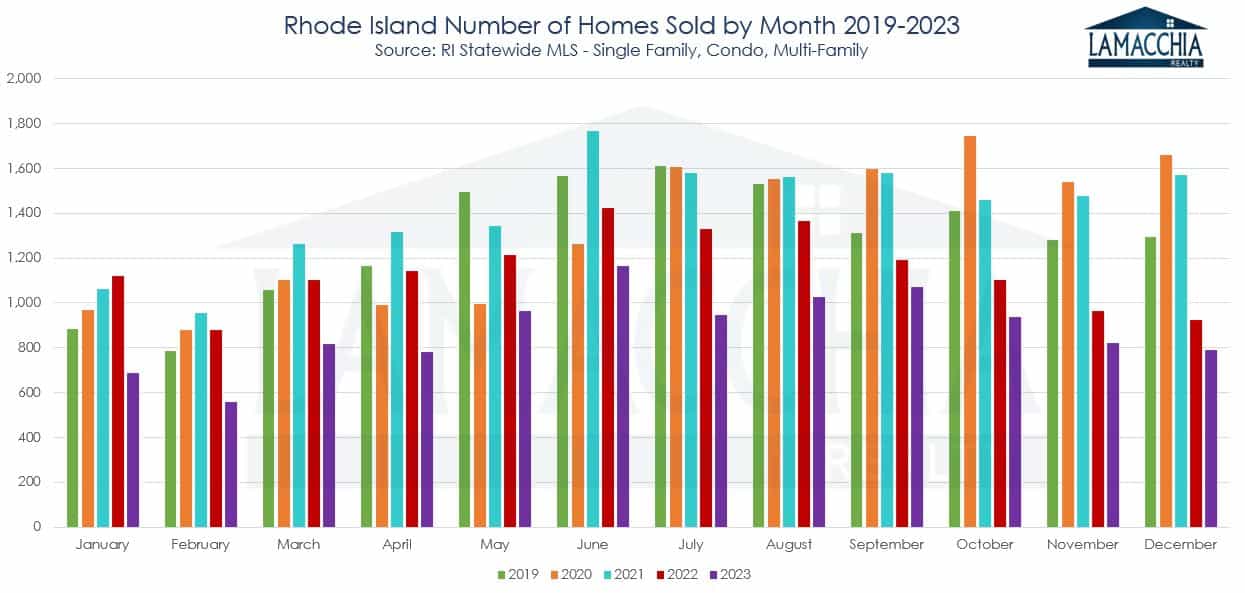

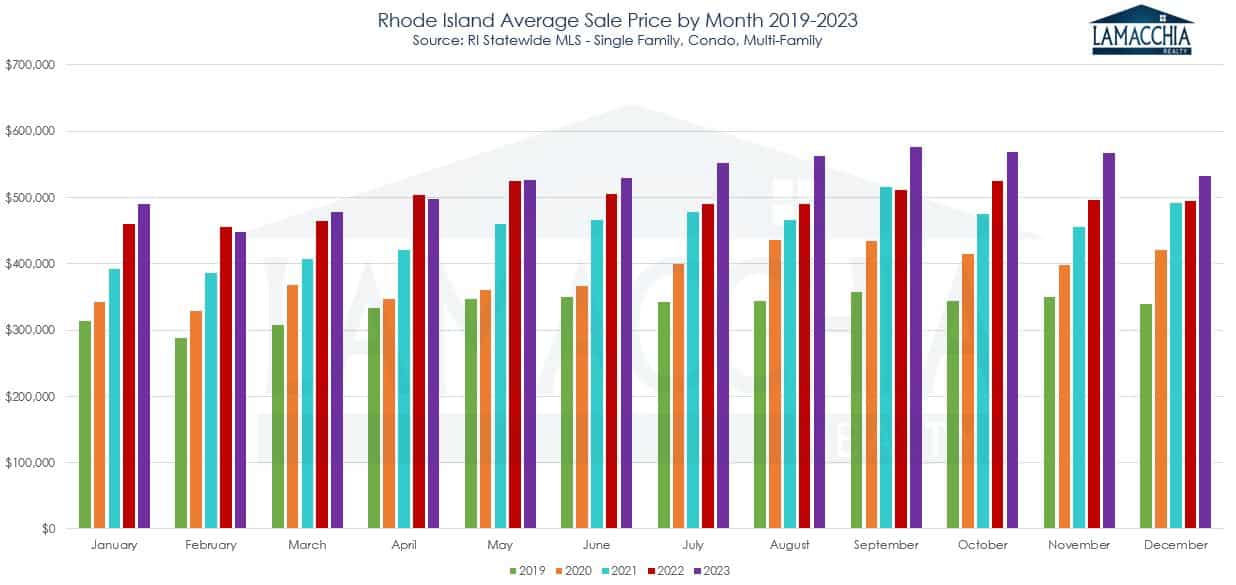

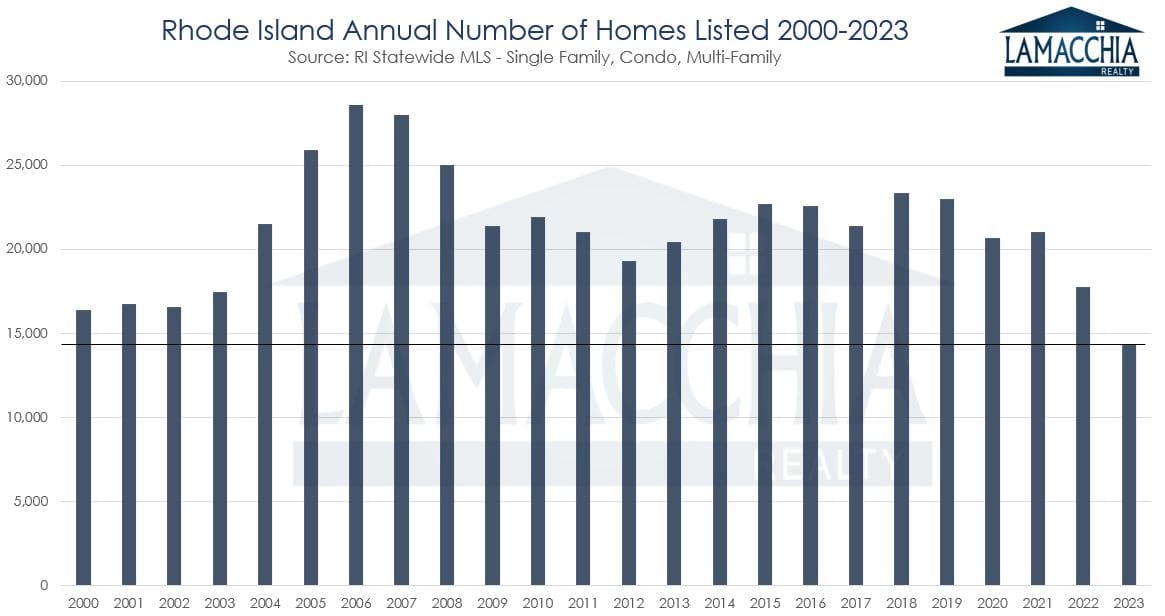

In 2023, the Rhode Island real estate landscape underwent significant changes. A standout element was the unprecedented low number of homes listed; a trend not observed in over two decades. This resulted in an acute shortage of available properties, leading to another year of increased prices. However, it also translated into a notable 23.2% reduction in sales, leaving prospective buyers eager to make a move. As interest rates sought to stabilize following their sharp decline in 2020, both buyers and sellers had to acknowledge the end of the era of historically low pandemic-induced rates, and the beginning of higher monthly mortgage payments.

In 2023, the Rhode Island real estate landscape underwent significant changes. A standout element was the unprecedented low number of homes listed; a trend not observed in over two decades. This resulted in an acute shortage of available properties, leading to another year of increased prices. However, it also translated into a notable 23.2% reduction in sales, leaving prospective buyers eager to make a move. As interest rates sought to stabilize following their sharp decline in 2020, both buyers and sellers had to acknowledge the end of the era of historically low pandemic-induced rates, and the beginning of higher monthly mortgage payments.

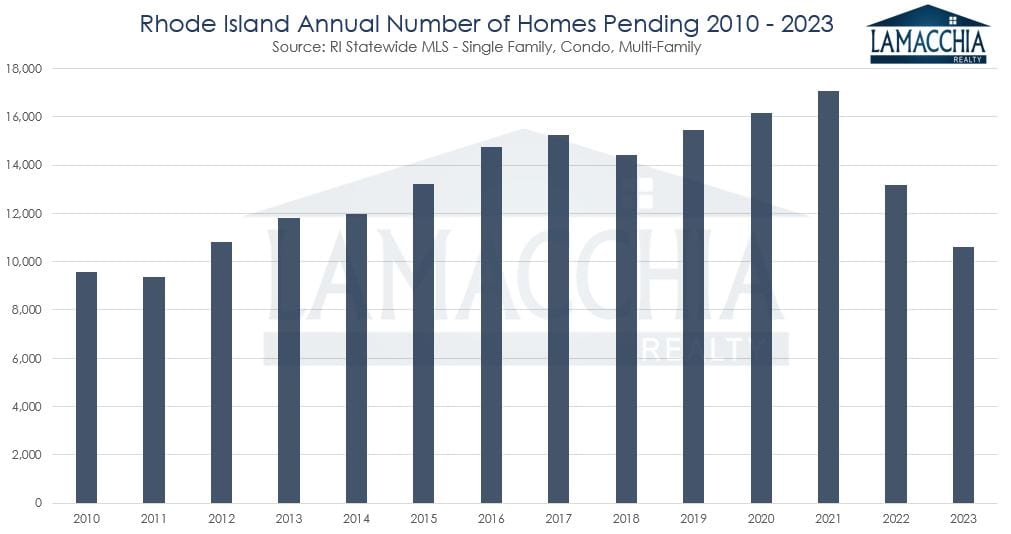

2022 also witnessed a decline in sales compared to 2021, accompanied by attention-grabbing headlines that fueled concerns about an imminent market crash. However, Anthony made it clear at that time that such an outcome was unlikely. Fast forward to the present, and no crash has occurred. The market’s resilience can be attributed more to the decrease in inventory than the decline in sales. The dip in sales in 2022 was not surprising but rather a relief, considering the unsustainable frenzy of the 2021 market. The subsequent year’s slower market activity reflects a shift towards equilibrium. Despite the necessity of a market adjustment, the process can be painful, and 2023 was undoubtedly a challenging year for all involved.

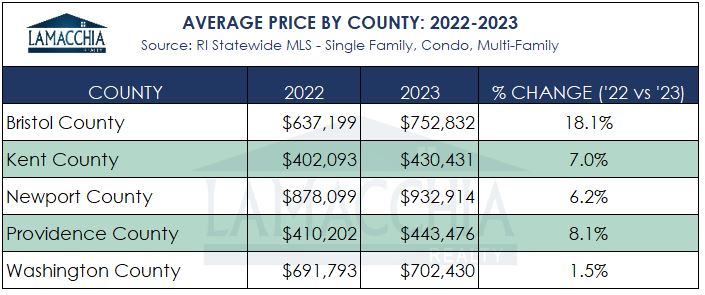

This report, the first one we are publishing for Rhode Island, examines sales, average prices, the number of active listings, and listings under contract for 2023 compared to 2022. Additionally, it provides predictions for what is anticipated to unfold in real estate in 2024.